Choosing where to live is one of the biggest financial decisions you’ll make each year. Get the rent number right, and everything else in your budget falls into place. (RENT calculator)Get it wrong, and you’ll be juggling bills before the month is even half over. That’s exactly why a rent calculator has become such a popular first step for renters in Australia ,it gives you a quick, realistic answer to “how much rent can I actually afford?” before you sign anything.

This guide walks through what a rent calculator does, how to convert between weekly, fortnightly, and monthly rent, and how to build a budget that holds up even when life throws in a few surprises.

Visit Now: https://rentcalculatorpro.com/

What Is a Rent Calculator?

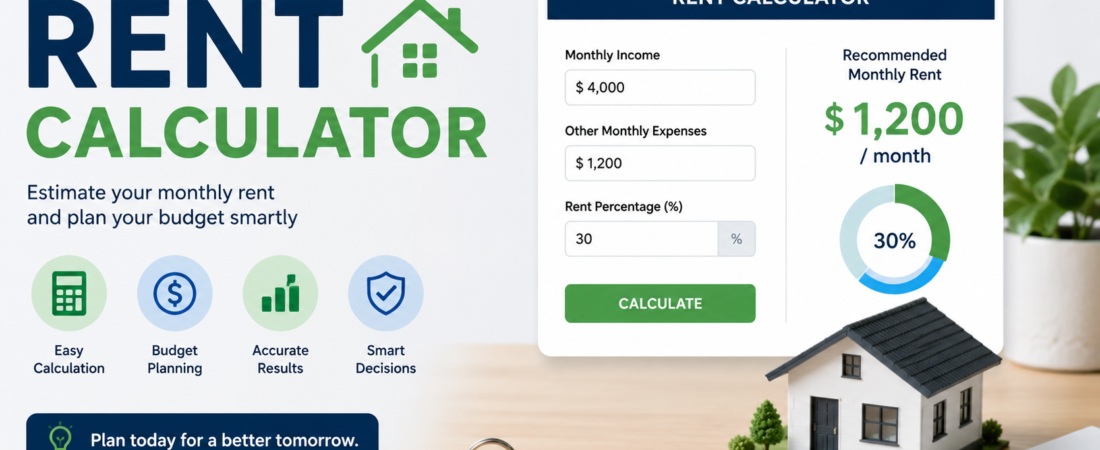

A rent calculator is a simple tool that estimates how much rent fits comfortably into your budget, based on your income. Most calculators lean on the 30 percent rule ,the long-standing guideline that no more than 30% of your gross monthly income should go toward rent.

It’s not a hard law, but it’s a useful starting point. The rule states that if you earn $5,000 a month, your rent should be $1,500 or less, with the rest being used for bills, savings, and day-to-day expenses.

Why a Rent Calculator Actually Matters?

It’s easy to fall in love with a property and stretch your budget to make it work. The problem shows up later, usually around the third week of the month, when the bank balance doesn’t match the bills still coming in.

A RENT calculator helps you avoid that by:

- Giving you a realistic budgeting starting point

- Highlighting how much room is left for everyday expenses

- Helping you compare properties on more than just “nice photos”

- Reducing financial stress before it becomes a real problem

A Sample Monthly Budget

Here’s how a $5,000 monthly income might be split using the 30 percent guideline:

Rent: $1,500 Utilities: $250 Food: $600 Transport: $300 Insurance: $250 Savings: $700 Entertainment: $300 Miscellaneous: $1,100

This kind of split keeps rent from swallowing your whole paycheque while still leaving room to save and cover the unexpected. It’s just one example ,your own numbers will shift depending on where you live and what your lifestyle looks like, but the structure is a solid template to start from.

Converting Weekly Rent to Monthly Rent

A lot of leases in Australia are quoted weekly, which makes it harder to compare against a monthly income or a monthly budget. Converting between the two isn’t complicated once you know the right multiplier.

Why Convert at All?

- It makes budgeting against a monthly income far easier

- It lets you compare two properties listed in different formats

- It gives you a clearer picture of your annual rent cost

- It helps with general financial planning

The Formula of RENT calculator

Since there are 52 weeks in a year and 12 months, the correct conversion factor is 4.33, not 4.

Monthly rent = Weekly rent × 4.33

A lot of people simplify this to “weekly rent × 4,” but that only accounts for 28 days ,and most months run 30 or 31. Using 4.33 keeps the number accurate rather than slightly underestimating your real monthly cost.

For example, $400 a week works out to roughly $1,732 a month ,not $1,600, which is what the “×4” shortcut would give you.

How Much Rent Can You Afford Based on Income?

As a rough guide, here’s how affordable rent tends to scale with income, using the 30 percent rule:

- $1,000/month income → around $600 rent (note: this exceeds the 30% guideline and works only with minimal other expenses)

- $3,000/month income → around $900 rent

- $5,000/month income → around $1,500 rent

These are starting estimates, not fixed rules. Your actual comfortable number will depend on your existing debts, dependents, and how much you want to save each month.

The 50/30/20 Rule (A Useful Companion to the 30% Rule)

Beyond just rent, many financial planners recommend a broader 50/30/20 budget split:

- 50% on needs ,rent, groceries, transport, utilities

- 30% on wants ,entertainment, dining out, travel

- 20% on savings or debt repayment

Used alongside the rent calculator, this gives you a full picture of your finances, not just the rent line.

Renting at Different Income Levels

Lower income earners generally have less flexibility, so picking a rent that’s comfortably within budget ,rather than at the very top of what’s “approved” ,matters more.

Middle-income renters tend to have a bit more flexibility when it comes to choosing a place, but that flexibility can backfire if budgeting gets skipped. Just because a higher rent is technically approved doesn’t mean it’s the smart move ,and a lot of people end up overcommitted simply because they never sat down and ran the numbers.

Higher earners obviously have more cushion to work with, but that cushion disappears fast without a plan. It’s actually pretty common for people on solid incomes to end up with little or nothing left at the end of the month ,not because they’re earning too little, but because nothing was being tracked in the first place.

Smart Budgeting Tips for Renters

Start by actually looking at where your money goes each month. Most people don’t blow their budget on one big purchase ,it’s the small, repeated stuff (coffee runs, subscriptions, takeout) that quietly adds up and throws everything off.

- Build a small emergency fund so a gap between tenancies or an unexpected bill doesn’t put your rent at risk.

- Look past the listed rent price. Factor in electricity, gas, internet, parking, and strata or building fees.

- If rent increases are common in your area, build a small buffer into your budget now rather than being caught off guard later.

How Debt Affects What You Can Afford

If you’re already paying off a car, student loan, or personal loan, those repayments reduce how much income is actually free for rent. (RENT calculator)A rent calculator based purely on income won’t account for this ,so it’s worth manually trimming your “affordable rent” number if you’re carrying other debt.

Tips for Finding the Right Rental

- Compare rent prices across a few suburbs before settling ,the difference can be larger than expected.

- If splitting costs with a roommate or co-tenant works for your lifestyle, it’s worth considering ,it can open up options that wouldn’t otherwise fit the budget.

- Keep an eye on “extra” amenities; a gym, pool, or covered parking might sound nice, but they’re often the reason a listing costs more than a near-identical one down the street.

- Don’t forget commute costs. A place that looks cheaper on paper can end up costing just as much once petrol, tolls, or public transport fares get added in.

Common Mistakes to Avoid

A few patterns show up again and again with renters who end up stretched thin:

- Falling for a property because it looks great, without checking what it actually costs to live there

- Forgetting that electricity, water, and other bills exist outside the rent itself

- Assuming rent will stay the same forever, instead of planning for it to go up

- Counting on bonuses or irregular extra income to justify a rent that’s otherwise too high

- Not having any emergency fund to fall back on

Steering clear of just these five mistakes puts most renters in noticeably better financial shape within a year.

Conclusion

At the end of the day, affordable rent isn’t just a percentage on a calculator screen ,it’s a decision tied to your income, your debts, your savings goals, and the kind of lifestyle you actually want. (RENT calculator) A rent calculator is a great starting point for that conversation, but the real value shows up when that number gets paired with a budget you’ll genuinely stick to.

Whether you’re comparing weekly listings against a monthly income, or just trying to figure out what’s realistic before you start inspecting properties, running the numbers first can save you months of financial stress later.

FAQ’s

1. Should I calculate affordable rent based on gross income or take-home pay?

Most rules of thumb, including the 30 percent guideline, are based on gross income simply because that’s the easier number for a calculator to work with. But your actual rent payment comes out of what lands in your bank account after tax. It’s worth running the numbers both ways, because relying on gross income alone can make a rental look more affordable than it really is once tax, super, and other deductions are taken out.

2. Does a rent calculator account for bills like electricity and internet?

No, and this is one of the most common mix-ups. A rent calculator only tells you what to spend on rent itself, not the full cost of living in a property. Two homes with the same rent can end up costing very differently once you add things like heating, water usage, or a building’s internet setup. Always treat the calculator’s number as a starting point, not the full picture.

3. Is the 30 percent rule still realistic in 2026?

In a lot of cities, rents have climbed faster than wages, so sticking strictly to 30 percent isn’t always possible without compromising on location or property size. The rule still works well as a benchmark for comparison, but plenty of renters end up somewhere between 30 and 40 percent depending on where they live. The key is knowing how far you’re stretching, rather than ignoring the number altogether.

4. Can a rent calculator help me negotiate rent with a landlord?

Indirectly, yes. If a calculator shows that a listed rent sits well above what’s reasonable for your income, that’s useful leverage going into a conversation with a landlord or agent. It won’t replace research into comparable rents in the area, but it gives you a clear number to anchor your negotiation around instead of guessing.

5. What if my rent calculator result doesn’t match what I can actually afford?

This happens more often than people expect, usually because the calculator doesn’t know about your personal debts, family size, or savings goals. Think of the calculator’s output as a generic benchmark. If your own budget tells a different story once you account for loan repayments or other commitments, trust your own numbers over the general guideline.

6. Should couples or share-house renters calculate affordability differently?

Yes. Most rent calculators are built around a single income, so if you’re splitting rent with a partner or housemates, you’ll need to combine incomes and divide the rent proportionally rather than applying the 30 percent rule to just one person’s earnings. This usually allows for a higher total rent while still keeping each person’s individual share reasonable.

7. How often should I recheck my rent affordability?

It’s worth revisiting the numbers whenever your income changes, a lease is up for renewal, or you take on new debt like a car loan. Rent affordability isn’t a one-time calculation, a number that worked comfortably a year ago might not hold up if expenses have crept up since then.

8. Does a higher credit score affect how much rent I can get approved for?

In many cases, yes. Landlords and rental agencies in Australia often check credit history alongside income when approving an application, and a stronger credit profile can sometimes make up for a slightly higher rent-to-income ratio. That said, approval isn’t the same as affordability, just because you’re approved for a certain rent doesn’t mean it fits comfortably into your monthly budget.

9. Is it better to rent below my calculated limit even if I can technically afford the maximum?

Generally, yes. The 30 percent figure is an upper limit, not a target to aim for. Renting slightly under your calculated maximum leaves more breathing room for savings, debt repayment, or unexpected costs, and it tends to make month-to-month budgeting noticeably less stressful.

10. Can rent calculators be used for commercial or business leases?

Most rent calculators, including the 30 percent rule, are designed around personal income and residential leases. Commercial rent is usually assessed very differently, often based on projected business revenue, foot traffic, or industry-specific benchmarks, so the same affordability formula doesn’t really translate.

11. What’s a reasonable rent-to-income ratio if I have no other debts?

If you’re debt-free, you often have more flexibility than the standard 30 percent guideline suggests, since more of your income is free to allocate toward rent without affecting savings. Even so, going much above 35–40 percent starts to limit your ability to save or handle a sudden expense, so it’s worth being cautious even without other debt pulling at your budget.

12. Do rent calculators factor in bond or security deposit costs?

No, a rent calculator typically only estimates the ongoing monthly or weekly payment, not the upfront costs of moving in. Bond, advance rent, and moving expenses can add up to several weeks’ worth of rent right at the start, so it’s worth budgeting for that separately rather than assuming the calculator’s number covers everything you’ll need upfront.